RESP Canada Toronto: A Simple Guide for Families

Book a free consultation · Family financial planning Toronto · Financial services hub

Why many Toronto parents search for RESP Canada Toronto help

RESP Canada Toronto is a common search for new parents here. It shows a real need. You want clear steps, a local view, and less stress.

Raising a child in Toronto costs a lot. School after high school can feel out of reach. Small moves now can change that path. This guide keeps the steps short and clear.

You may fear complex rules, fees, and fine print. You might not know which bank to use or when to start. I will walk you through each choice.

Here is the main point: start early, use grants, keep fees low, and let money grow for school.

In this guide, I share how the plan works and how to claim grants. I list places to open an account in Toronto. I compare plan types. I offer simple steps to fund and invest. I end with tax rules and key traps to avoid.

I am Caroline Arcos Vasquez. I help families and small firms in Toronto with financial solutions, life planning, and visa support. I write in plain words and link to sources you can trust.

Keep one aim: small, steady moves. They add up over time. The RESP is a tool, not a race.

What RESP Canada Toronto means and how it works

An RESP is a tax-smart plan for school. It helps you save for a child’s future. RESP Canada Toronto is how many families find this plan near home.

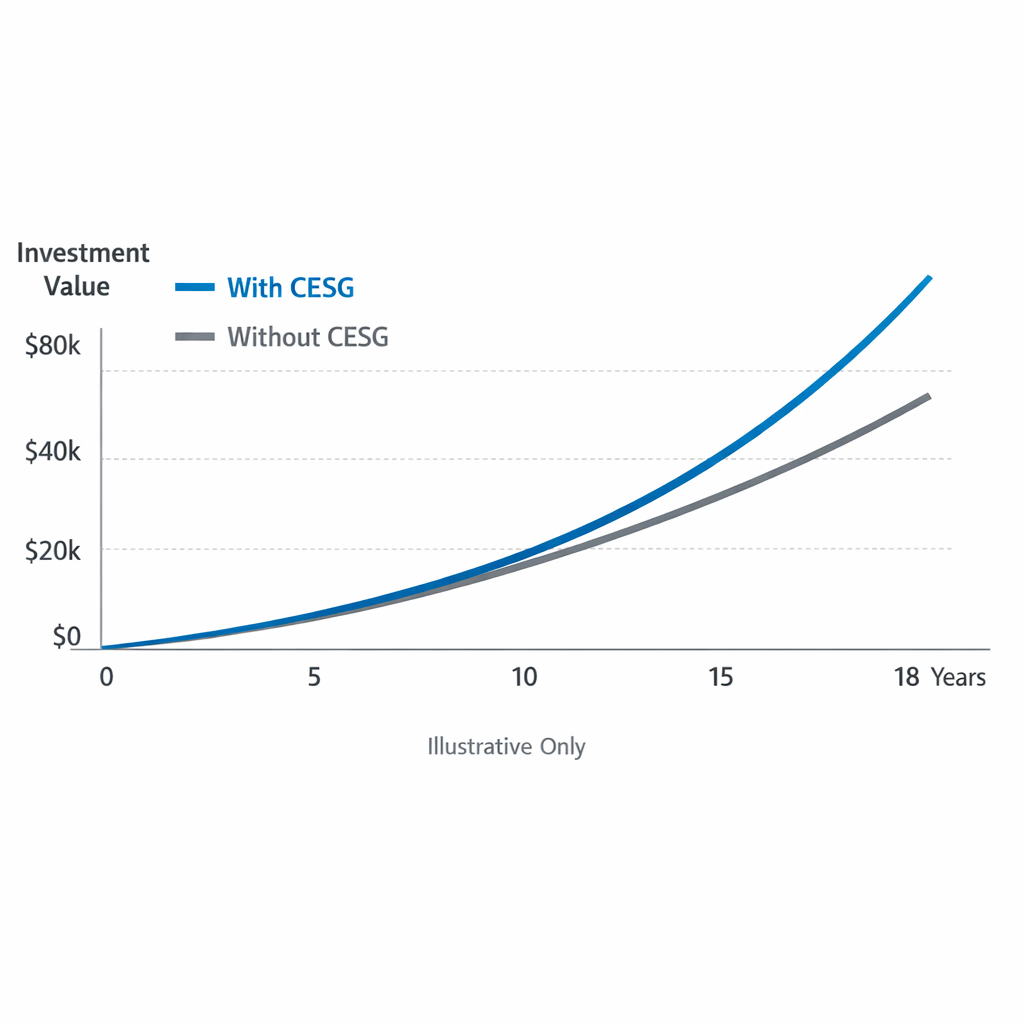

Here is the core idea. You put money in the plan. The plan can grow tax-free while it stays in the account. The government may add grants on top. That stack lifts your savings.

The Canada Revenue Agency has a clear page on RESPs. Read the CRA RESP overview for rules, taxes, and who can open one.

You can open an RESP for your child, a niece, or a grandchild. In Toronto, banks, credit unions, and online firms can help set it up. Each needs ID proof and the child’s SIN.

The main draw is the grant. The Canada Education Savings Grant (CESG) adds 20 percent on yearly deposits up to a set cap. The Canada Learning Bond (CLB) can add funds for low-income households. I link both below so you can check the rules.

When the child goes to school after high school, you take the money out. Part is your own money. Part is growth and grants.

Growth and grants are taxed to the student, not you. Many students pay little tax because income is low in those years. For broader savings context, see family financial planning Toronto.

Terms to know

- Subscriber: person who opens and funds the plan.

- Beneficiary: the child who will use the funds.

- EAP: the grant and growth part paid to the student.

Why this matters in Toronto

School costs keep rising. A plan with grants can ease that load. A small start now beats a big start later. Local RESP help can make the start quick and clean.

“An investment in knowledge pays the best interest.”

- Benjamin Franklin

That line still rings true. It sums up why we use this plan.

RESP Canada Toronto grants: CESG and CLB for families

Grants are why RESPs shine. They are real money. They help your savings grow faster than on your own. Many Toronto parents read this section to learn which grants fit.

The CESG adds 20 percent on the first chunk you put in each year. The yearly cap for this match is $500 per child. The lifetime grant cap is $7,200 per child. You can read more on the official page: Canada Education Savings Grant. That page shows who can get the base and extra match.

There is also the CLB. It helps low-income households start to save. The CLB can add up to $2,000 per child over time. It pays $500 to start, then $100 for each year you qualify, up to age 15. Check the rules on the Canada Learning Bond page. You do not need to add your own cash to get the CLB.

How to get the grants

- Get a Social Insurance Number for the child.

- Open an RESP with a bank or a firm.

- Ask the firm to apply for CESG and CLB on your behalf.

The firm files the grant forms. You do not mail forms to Ottawa. However, you must give consent and the child’s SIN. That is why set up steps matter.

Why speed counts

Grant room builds each year. If you start late, you can catch up part of it. But there is a cap on how much grant you can get in one year. So start now if you can. Small, steady cash can earn the full yearly match.

For Toronto homes, the CLB is a help. Some banks will help you get the CLB with no deposit. Ask for this when you open the plan. A local advisor can smooth the steps.

Where to open an RESP in Toronto: banks and online brokers

You can open an RESP in many places in Toronto. Your choice can change costs and fund options. Many families start with banks first. Banks are easy to reach and have branches near you.

Big banks offer RESPs with funds and GICs. For example, see RBC RESP and TD RESP. These pages explain how to start and the types of funds they sell. They can also help with CESG and CLB forms.

Online brokers give you more fund choice and low fees. One example is Questrade RESP. With a broker, you can buy index ETFs. Fees can be low, but you must pick and manage the mix. That takes a bit of time.

Credit unions in the GTA can be a nice middle path. They know local needs. They often have GICs with fair rates. Ask about fees and grant help.

What to ask before you sign

- What are the annual fees for the account?

- What are fund fees (MER) for the choices I can buy?

- Can I buy low cost index funds or GICs here?

- Do you file CESG and CLB forms for me?

Get these answers in plain words. If the rep sells high fee funds only, ask for an index fund list. If they will not share, keep looking. Toronto has many RESP providers and plan types.

Trade-offs to weigh

- Branch help is warm, but funds may cost more.

- Online brokers are cheap, but you must do more tasks.

- Credit unions know local needs, but choices can be fewer.

Your best path is the one you will stick with. A low cost plan you fund each month beats a complex plan you avoid. Pick ease and cost in balance. I can help you compare options side by side.

Pick the right plan: individual, family, or group

Plan type shapes how you save and how you share funds. RESP Canada Toronto guides usually list three plan types: individual, family, and group. Here is what they mean in short form.

An individual plan has one child as the beneficiary. A family plan can have more than one child, but all must be linked by blood or adoption to the subscriber. Group plans pool many families together under a promoter’s rules. Not sure where to start? Insurance planning Toronto is a calm first step before you open accounts.

Here is a quick table to compare.

| Plan type | Who it fits | Key pros | Key cons |

|---|---|---|---|

| Individual | One child, non-related child, or unsure on more kids | Simple, flexible | No sharing with siblings |

| Family | Two or more kids in one home | Share growth and grants across kids | Must be related to you |

| Group | Sold by promoters with set rules | Forced saving habit | Fees, strict rules, lower flexibility |

Group RESPs can sound good, but there are strict rules. The Ontario Securities Commission warns to read terms and fees with care. See OSC on group RESPs.

If you miss set payments, you may lose some money to fees.

Why most families choose individual or family plans

They are clear. They are flexible. You set the amount and timing. You pick the funds. You can move firms if fees get high. In a group plan, that is hard or costly.

“Education is the most powerful weapon which you can use to change the world.”

- Nelson Mandela

This quote fits the heart of the plan. We save so our kids have more paths.

A note on blended homes

Family plans need kids who are related to you. Step and adopt ties can count. Ask the firm to check the rule. If in doubt, open an individual plan for each child. It is simple and safe.

A local advisor can guide this choice. Bring your family plan, if any. We can match the plan type to your path.

How to fund and invest: steps for a low stress start

You set up the plan. Now fund it and set the mix. Keep this part plain and calm. Here is a small plan you can use.

A simple five step start

- Pick an auto deposit you can keep.

- Aim for $2,500 per year for full CESG.

- Use one or two index ETFs or a GIC.

- Rebalance once a year.

- Shift to safer funds as school nears.

Small, steady cash is the key. You do not need a big lump sum. Auto deposits make it a set and forget move. They also help you get the full CESG match each year.

GICs vs index funds

GICs are safe. Your cash will not drop in value, but growth may be low. Index funds carry more risk and can drop for a while. Over the long run, they often grow more. The Financial Consumer Agency of Canada has plain-language guides on savings and funds.

A mix can work well. For a child age two, you might use more index funds. For a child age 16, use more GICs and cash. That way, when you need the money soon, it is there.

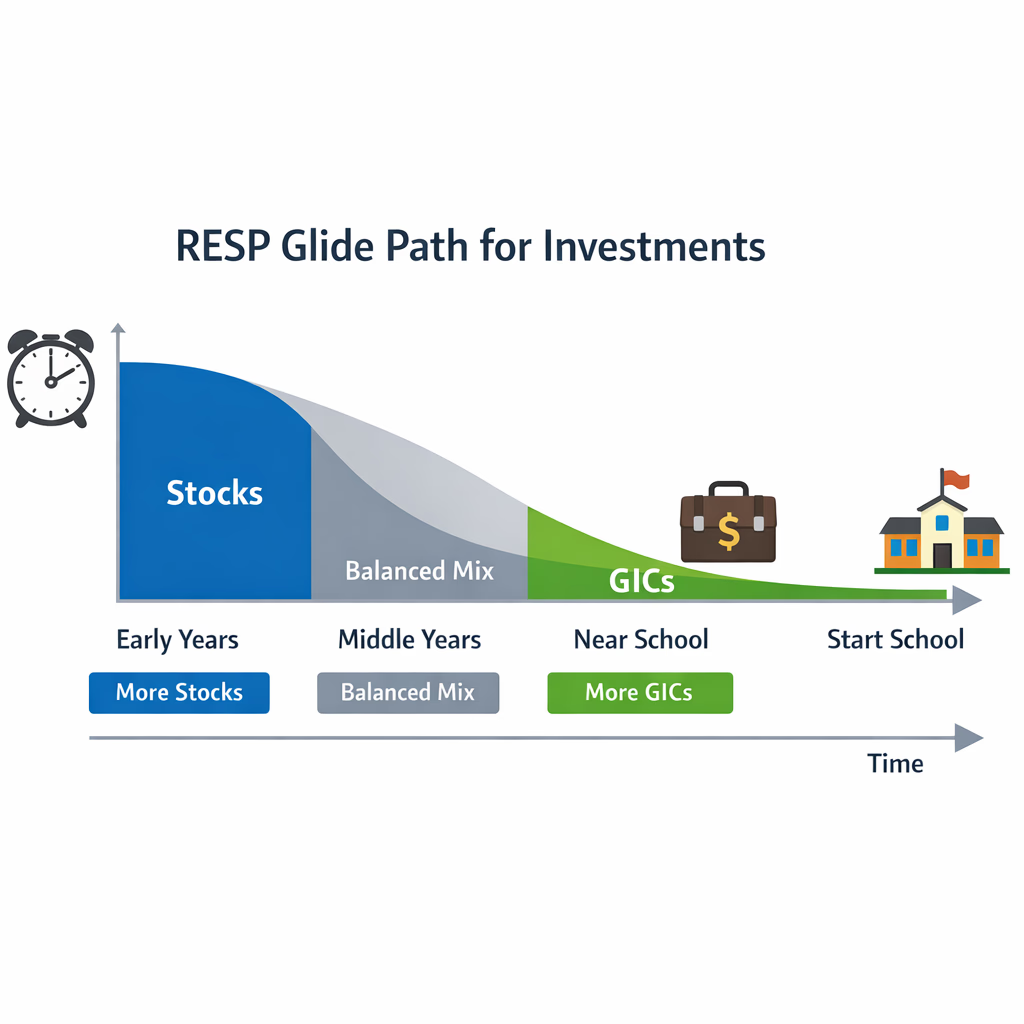

A sample glide path

- Age 0 to 10: 70 to 80 percent index funds, rest in GICs.

- Age 11 to 14: 50 to 60 percent index funds, rest in GICs and cash.

- Age 15 to 17: 20 to 30 percent index funds, rest in GICs and cash.

This is not a rule. It is a start point. Your risk and needs may differ. Your RESP plan can be shaped to your path. I can help tune the mix.

Tips to avoid stress

- Check fees. Fund fees eat growth each year.

- Use auto deposits. You will not forget a month.

- Keep the mix simple. One or two funds are enough.

Keep your plan in a folder or app. Review once a year. Make one or two small tweaks. Then get back to life.

Tax, withdrawals, and big mistakes to avoid

Tax rules can sound hard. Let’s make them easy. This section cuts the noise and shows the key parts.

You have two kinds of cash in the plan. First is your own cash. That part is not taxed when you take it out. Second is growth and grants. That part is called EAP. It is taxed to the student, not you. Many students pay low tax, so EAP can be light on tax.

In the first 13 weeks of school, there is a cap on EAP per child. After that, the cap rises.

Check the CRA RESP page for exact EAP limits and forms. Firms know these caps and can guide withdrawals.

Big mistakes to avoid

- Missing grant room by skipping years.

- High fee funds that eat gains.

- Locking into strict group plans you do not need.

- Taking all EAP too fast and paying more tax than needed.

- Forgetting to use funds within the time window.

The plan can stay open for many years. If your child does not go to school right away, do not rush. You have time. If no child uses the plan, there are rules to move some growth to your RRSP if you have room. Check the CRA link for those cases.

Move or study abroad

If your child goes to a school outside Canada, the plan can still help. The school must be on an approved list. Ask your firm to check. If you move out of Toronto or Canada, you can still hold the plan. Keep your address up to date.

A quick checklist for withdrawals

- Get proof of enrolment from the school.

- Ask the firm to pay EAP first when tax is low.

- Pace EAP over the years of school.

A withdrawal plan can save tax and stress. I can help you set a year-by-year pull plan.

Toronto specific help: newcomers, bilingual support, and busy parents

Toronto is diverse and fast-growing. Many households move here with big goals. RESP Canada Toronto help should fit that mix. My work is to make the plan fit your life, not the other way around.

Newcomers and visa status

Newcomers can open an RESP once the child has a SIN and you have status. If you need help on travel or visa steps, see travel insurance Toronto and my visa support. We can time the RESP start to your status and SIN steps so grants are not delayed.

Bilingual help

I speak English and Spanish. We can talk in the language you prefer. See bilingual insurance Toronto for how consults run. We use plain words and clear steps, not jargon.

Busy parents and small firms

Time is short. So we set a one-hour plan chat. Then we split tasks into small steps. I can help set auto deposits and a yearly check-in. You do not need to watch the plan each week. Keep it light and calm.

“Simplicity is the ultimate sophistication.”

- Leonardo da Vinci

I like that line for money plans. Simple plans work. Complex ones break.

You can also link to city help. Community centres host tax and grant clinics at times. Check local sites and libraries. They may help you apply for the CLB on set days.

What this means for your child

A plan is not just money. It is a story you tell your child. You can say, we set this up for you. We believe in your path. That can lift a child in real ways.

Words to use when asking for RESP Canada Toronto help at a bank

Talking to a bank can feel hard. Here are short lines you can use. Print this list. Take it to the branch. These lines make sure you get what you need.

- I want to open an RESP for my child in Toronto.

- Please add the CESG request to my file today.

- Can you check if my child can get the CLB?

- Show me your lowest-fee index fund choices.

- What are the MERs and any account fees?

- Can I set a $210 auto deposit each month?

- Please explain how to take EAP when school starts.

- How do I move this RESP if fees rise?

These lines keep the talk on track. They also show the rep you plan to use grants and keep fees low.

A short role play

- You: I want low fee options. What is your total MER?

- Rep: Our balanced fund MER is 2 percent.

- You: Do you offer index ETFs or a cheaper balanced fund?

If the rep will not offer low fee paths, thank them and leave. You can open your RESP at a place that fits your needs. Your child’s future is worth that care.

Words vs actions

Here is a small table to link words to steps.

| Words you say | Action they should take |

|---|---|

| Add CESG and check CLB | File grant forms with your consent |

| Low fee index funds | Show ETF or index fund list with MER |

| Auto deposit | Set monthly transfer from your bank |

| EAP plan | Note a plan to pace EAP across years |

Keep this table on your phone. It helps you test if the firm will do the work you asked for.

A local plan you can start this week

You do not need months to start. You can do the core steps in one week. RESP Canada Toronto is not just a search term. It is a plan you can start now.

A one week path

- Day 1: Get your child’s SIN if you do not have it.

- Day 2: Pick your firm and book a short call.

- Day 3: Open the RESP online or in branch.

- Day 4: Set a $210 per month auto deposit.

- Day 5: Pick one index ETF or a GIC.

- Day 6: Ask for the CESG and check the CLB.

- Day 7: Save the plan file and set a yearly date.

This path fits busy lives. If you need help, I can book a call to do steps with you. We can do it in English or Spanish. We keep it warm and simple.

A Toronto view on cost of school

Costs move over time. It is hard to pin one number, so plan for a range.

Some kids will do a two-year college. Some will do four years at a university. Some will do both. Use grants to boost your base. Use low fees to keep more growth.

Read the base rules on the CRA RESP overview. Cross-check grants on CESG and CLB. These are official links.

Your plan can flex. We can change the deposit or mix as life shifts. We can pause if work hours change. We can raise cash in a bonus month. The plan bends to your life.

Key takeaways

- Start now with what you can.

- Use CESG and check CLB.

- Keep fees low and steps simple.

- Pace EAP to the student’s tax.

That is the heart of this plan. Small moves. Big impact.

What to do next in Toronto: book a calm plan chat

We covered a lot. Here is the short view. RESP Canada Toronto help is close at hand. Start the plan, grab the grants, keep fees low, and pace withdrawals at school.

If you feel stuck, that is fine. This is new. Book a free insurance consultation. I can help you open the plan, pick low-fee funds, and set auto deposits. I can also help you ask the right questions at a bank.

Newcomers have more steps. I also help with travel and visa support. We can time the RESP start to your SIN and status path. If you speak Spanish at home, we can hold the chat in Spanish.

Your child’s path starts with one small act. Open the plan. Set a tiny deposit. Ask for grants. Then take a breath. Calm, steady moves beat stress.

If you want a full review, bring this to our chat:

- Your child’s SIN.

- Your monthly budget range.

- A note on your risk comfort.

- Any bank you prefer to use.

We will make a plan you can live with. No hard sell. No pressure. Just clear steps and care.

In the end, the goal is choice. School should be a door that opens wide. Your plan can help turn the knob. RESP Canada Toronto is more than a search phrase. It is a promise you can make real, one month at a time.

If you are ready, book a short call. If you need more info first, read the linked pages above. Browse more financial tips Toronto on the blog, then come back when you are set.